Courtesy of: Rafael Reyes, Originating Branch Manager at Cross Country Mortgage.

Troubles in the banking sector in the US and Europe completely overwhelmed the economic reports in driving financial markets this week. Investors shifted to safer assets, and mortgage rates moved lower.

The impacts of the largest bank failure in the US since the financial crisis in 2008, as well as serious issues at a second big US bank and a major European bank, were positive for mortgage rates for a couple of reasons. Since the issues developed mostly as a result of the rapid monetary policy tightening by the Fed to fight inflation, investors now are concerned to what degree other banks have similar problems and whether higher rates will cause cracks to emerge in other areas of the financial system. The reaction to this increased uncertainty was to shift from risky assets such as stocks to relatively safer ones such as bonds, including mortgage-backed securities (MBS). Added demand for MBS causes mortgage rates to decline. In addition, banks are expected to tighten their lending standards, meaning that it would be more difficult for businesses to obtain loans. This would slow economic growth, reducing the outlook for future inflation, which is also beneficial for mortgage markets.

On Thursday, the European Central Bank meeting may have provided a preview of how the US Fed will address the troubles in the banking sector at its meeting next week. Although the ECB had signaled at their prior meeting that they planned to raise rates by 50 basis points at this meeting, many investors anticipated that the banking sector troubles would result in a smaller 25 basis point increase to lessen the negative impact on banks. However, the ECB did raise rates by 50 basis points, while carefully drawing a distinction between its roles for maintaining price stability and for ensuring the safety of the financial system. The ECB stated that it was ready to provide liquidity to the banks if needed, but also stressed the need to aggressively fight inflation.

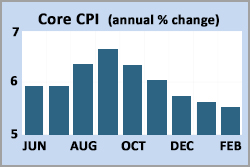

The latest key inflation data came in very close to expectations and caused little reaction. The Core Consumer Price Index (CPI) is a closely watched inflation indicator that excludes the volatile food and energy components. Core CPI in February was up 5.5% from a year ago, down from an annual rate of 5.6% last month. Shelter (housing) costs remained stubbornly high and again were responsible for the largest portion of the increase.

Even with all the dramatic economic news this week, the Retail Sales report on Wednesday still received some attention, since consumer spending accounts for over two-thirds of US economic activity. After a massive surge of 3.0% in January caught investors off guard, retail sales in February contained no major surprises, falling modestly from January as expected. In general, consumers spent more on necessities such as groceries, while cutting back at restaurants, auto dealers, and department stores.

Week ahead

By far the biggest event next week will be the Fed meeting on Wednesday, and most investors anticipate a 25 basis point increase in the federal funds rate. They will be closely watching to see how the Fed addresses the banking troubles and what guidance is offered on their plans for future rate hikes. It will be a light week for economic reports. Existing Home Sales will be released on Tuesday and New Home Sales on Thursday.

| Rafael Reyes Originating Branch Manager D 718-663-1236 F 347-329-1965 W Rafknowsrealestate.com E rreyes@ccm.com |

| CrossCountry Mortgage, LLC 37 N 15th Street, Suite 108 Brooklyn, NY 11222 Personal NMLS68976 Company NMLS3029 |